Everybody makes the same valuation mistake

They forget to factor the fade.

This summer I had the instructive experience of teaching my first business school class. The first lesson I learned was how much time it takes to prepare 21 hours of lectures on Corporate Valuation. It takes a long time even if you already know what you want to say.

A second lesson came from the exercise of grading the papers, which was that most valuations are too optimistic. I used to think that analyst valuations were all too optimistic because of some obvious bias in sell-side life. But perhaps it’s just that everyone is too optimistic? My class produced huge upsides to fair value and happily assigned Buy ratings. Their models were raining cash.

So I tried to figure out where their optimism was coming from. Over and again, it was coming from the same place. They forgot to factor the fade.

The fade is entropy. It’s the decay of everything over time and it impacts everything - from your car, which needs a service by the way, to my park run time. Businesses don’t get an exemption, and nor do their assets.

So if you are asked to come up with a set of company forecasts, here’s what you shouldn’t do: take last year’s accounts and apply a bunch of growth rates. Yes, if you plug in an assumption that revenues will grow by x%, costs by y% and therefore profits by z% … then congratulations, you will be operating perfectly within the logic of your spreadsheet. But you’ll simply produce what I saw a dozen times in the papers from my class: too much free cash flow.

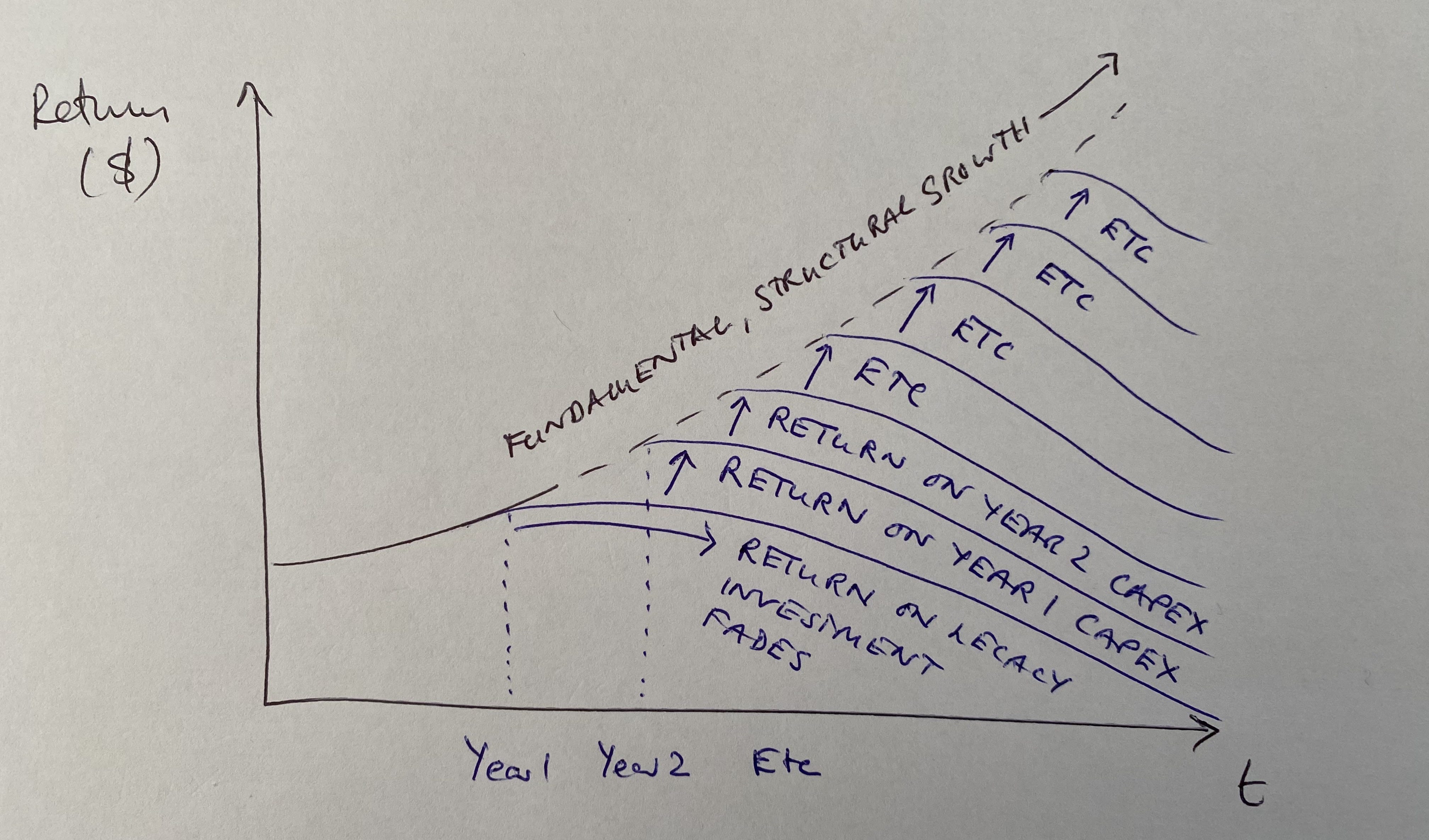

The antidote to the optimism disease is to focus on investment and return. For most businesses, one year’s investment drives another year’s return. Utilities need to build power plants. Retailers need to refurbish their stores. Tech companies need to write code. It’s even true for companies like law firms or consultancies which may not show much capital investment in their accounts - the low capex is just an artefact of how the accounting profession defines investment. (For these businesses, the investment is still taking place, it’s just captured in the opex line, in things like recruitment, mentoring, coaching, client development.)

So if next year’s profit comes from last year’s investment, what happens to last year’s profit? The answer is that, like the glow of youth, it fades away. It has to fade, as the invested capital (which produced it) depreciates. If capex = depreciation, then earnings can be flat. Or perhaps you can cut some costs and collect a one-time bump in profits from that. But for structural, fundamental growth, a business needs to be investing, at ROIC > WACC and usually at Capex > D&A. The picture should look a bit like this:

There’s a famous passage in Vergil’s Georgics, a long poem about humanity dressed up as an agricultural training manual, which perfectly captures the idea:

“I’ve seen choice seed, proven with much labour, degenerate still, if the largest were not picked out each year by human hand. So, all things are fated to slide towards the worst, and revert by slipping back: just as if one who can hardly drive his boat with oars against the stream, should slacken his arms, and the channel sweep it away downstream.” (Georgics Book I, 197 - 203, Translation by AS Kline)

If the greatest Roman poet could give us such a vivid picture of how forward progress struggles against backward entropy, then we should do our best to remember it. So when preparing a valuation, or a valuation paper for class, remember to factor the fade. Allow that invested capital will depreciate; future returns will have to reflect new investments; and forecast a growth rate which reflects the balance of those two forces.

Remember, in other words, that all our endeavours row against the current, and the way to accumulate progress is with good investments. Whether companies succeed or are washed away downstream depends more than anything else on how much they are able to invest, and at what return.

CODA

The Vergil is better in the original. Here it is for the latinists out there.

Vidi lecta diu et multo spectata labore

degenerare tamen, ni vis humana quot annis

maxima quaeque manu legeret. Sic omnia fatis

in peius ruere ac retro sublapsa referri,

non aliter, quam qui adverso vix flumine lembum

remigiis subigit, si bracchia forte remisit,

atque illum in praeceps prono rapit alveus amni.

(Georgics I, 197 - 203, Perseus Digital Library)

Interesting post Sam. Nicely written also.

Fascinating stuff Sammie. Agree with Fred - really well written. Keep it coming!