Cosmic Principle No. 2

Something to think about as you finalise your New Year resolutions

Your email service resumes (after a Xmas break) with a 5 min read. And in case you have forgotten, the purpose of this column is to share, explore and celebrate ‘Good Ideas’ of any kind. Comments and suggestions always welcome. Thanks for being a reader… and Happy New Year!

Everybody knows that compound interest is a powerful thing.

But let’s test your intuition: how long would it take to double your savings, with a compound annual interest rate of 3%, 5% or 7%? And how long would it take, on average, to double your money in the US stock market? Think about it for a moment, and note your answer before you read on.

It turns out there is a useful rule of thumb to answer this question. If you start with the number 70 and divide by the interest rate, you will get 23, 14 and 10 years for the three examples I gave, which is close enough to the right answer - and probably a faster timeframe than you estimated, even if you already knew perfectly well about the power of compounding.

There is an explanation of how this shortcut works in the footnote.1 But more importantly, the exercise tempts me to propose another universal law, let’s call it Sam’s Cosmic Principle No. 2 (to follow on from last year’s Cosmic Principle No. 1) as follows:

Compounding is more powerful than you think, even if you already think compounding is more powerful than you think.

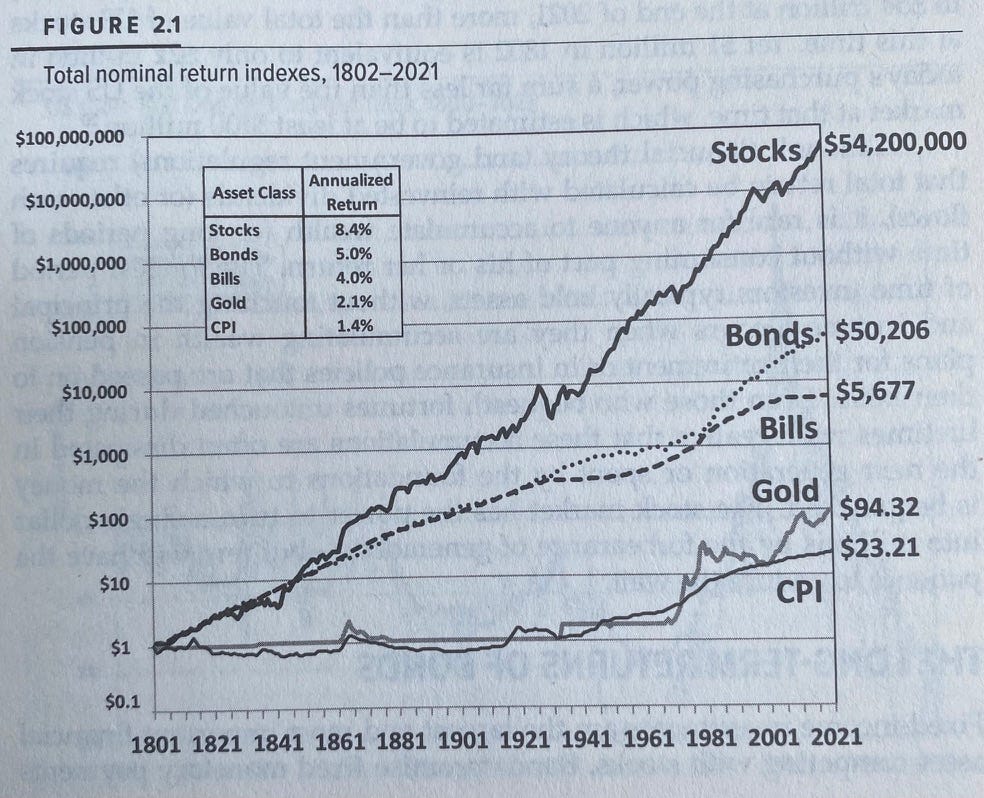

To test whether this makes sense, look at the US stock market example. Jeremy Siegel has shown that the long run, nominal return on US stocks averaged 8.4% annually, from 1801-2021 (see chart below). On that basis, our rule of thumb suggests investors will double their money in 70 / 8.4 = … a little more than 8 years. As Benjamin Franklin said: Money makes money, and the money that money makes, makes money.2

Does that surprise you? Of course, the stock market example is based on an average, and not every 8 year period is ‘average’. There are many ups and downs and investors are taking risk. But if you agree that it’s surprising to see that, on average, US stock market investments have doubled in value every 8+ years for more than two centuries, then you probably won’t object to my new law.

Which leaves us with the question, how can you use Cosmic Principle No. 2 to your advantage? Here are some ideas:

Financially, save and invest as early as you can in life. As the Chinese proverb goes: The best time to plant a tree is 20 years ago, but the second best time is now. So buy the market index in a low fee tracker and forget about it for as long as you can. Just make sure you don’t need the funds in a hurry, so you are not forced to sell at any particular time - and especially not in a downturn. (You might also think about timing your entry, but see this footnote first.3 )

Fund your early investments with frugality. A smart client once pointed me to an outstanding Cicero quote: “o di immortales!”, the great man said, “non intellegunt homines quam magnum vectigal sit parsimonia!” I would loosely translate that as: ‘By the immortal Gods! People don’t realise how much money they can make by saving!’ He was as usual making a very good point.

In this context, delaying spending can also be a helpful measure, so long as your investments are growing faster than inflation. Treat every pound as a prisoner. The general message, often relevant in business as well as personal life, is that you don’t need to pay for everything that needs doing. You just need to pay for what needs doing now.4

Outside of the family finances, you can also think about how compounding works to your advantage. I am generally not very good at compounding my trips to the gym, or my efforts to stop snacking, though the logic of this article suggests I should try harder on both.

Yet one area where the value of compounding never ceases to amaze me, and where I find my motivation much easier to tap into, is in friendships. Here, the bottom line is that compounding relationships makes life better. Why? Because what grows in relationships over time is mutual understanding and trust, and the more you have of each, the easier things become. You can anticipate what will happen next. You know what you each like. You can call for support when you need it. In a close relationship compounded over many years, you can agree on what to do next with a simple conversation, rather than with an army of lawyers and a complicated contract.

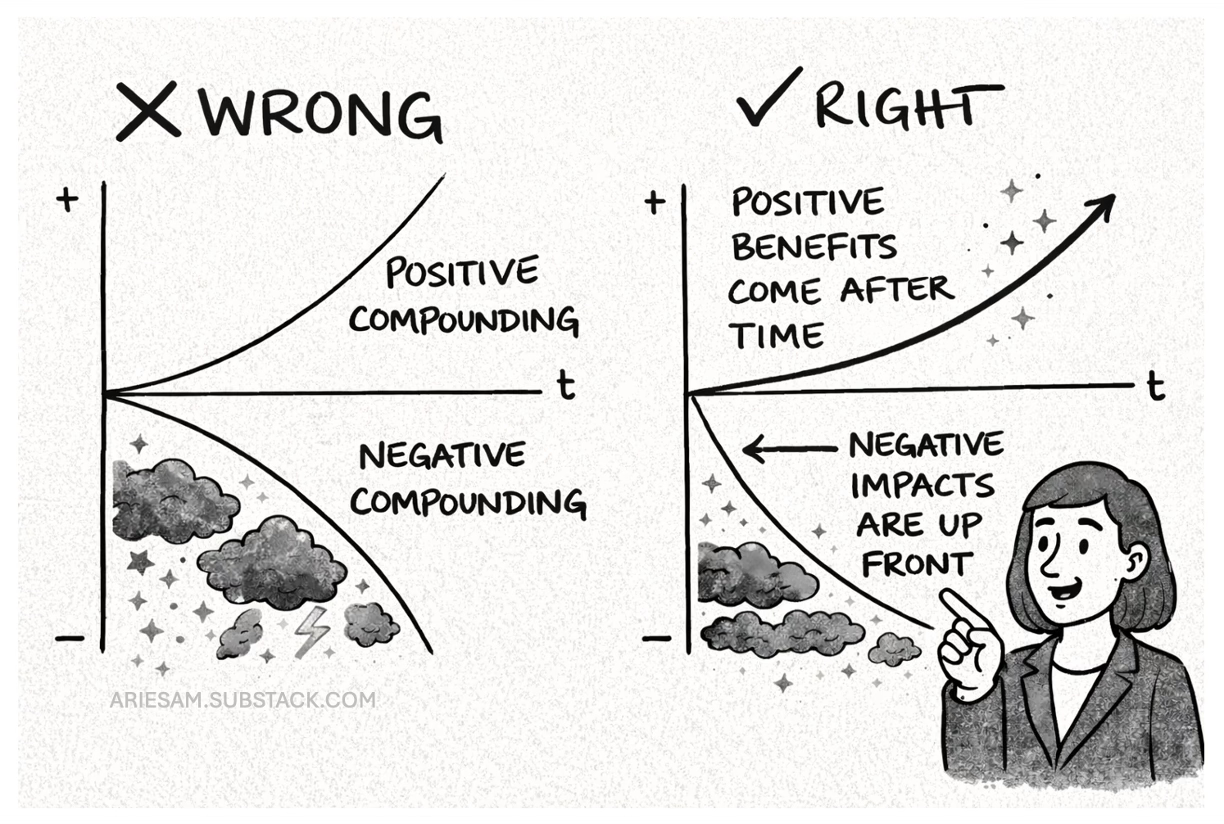

A final thought on the subject of compounding arises if you think about the shape of exponential growth (or decay) curves over time. It will be obvious that the incremental benefit of positive compounding increases over time. The rewards are inevitably back-loaded, one of the reasons perhaps that people generally report greater happiness in later life. But the opposite is true for the incremental costs of negative compounders, which are at their worst in the early days. The decay curve is not a mirror image of the growth curve, but a rotation of it - as shown below.

What this means in practice is that the greatest rewards from good habits (regular savings, careful investments, lifelong friendships) will come after a long wait, but the greatest losses from bad habits (which compound negatively over time) come early and up front. So if you want to achieve a balance in your New Year’s resolutions, it makes sense to think about a mix of adopting good habits for the future, and dropping the bad habits which have potential to hurt you right now. Taken together, those resolutions should give you a better balance of short and long term payback.

And with that, I’m off to the gym…. though I hasten to add, I may need to stop for a snack on the way.

Enjoyed this? Try these

Nato and 1984 (10 mins)

Cosmic Principle No. 1 (5 mins)

Is the AI bubble bursting now? (15 mins)

The Bad Good Idea (5 mins)

Bill Gates and Point Break (10 mins)

Life advice - from chess (5 mins)

The dumbest thing a Congressman said (12 mins)

The House Always Wins (5 mins)

The power of a pure idea: #1 - The Finger Space (10 mins)

Every cloud has a sulphur lining (5 mins)

We only have 5 things (5 mins)

Electric Vehicles and the Parable of the Magic Button (5 mins)

Advice for a college freshman (4 mins)

Our brains are not wired to understand geologic time (20 mins)

You’re the decision maker now (4 mins)

The most crowded trade in the City (5 mins)

An undiscovered Easter Egg in Stegner’s masterpiece (15 mins)

What we learn about Britain from the plunging barley price (4 mins)

The College Essay is dead - Long Live the ‘AI Viva’ (5 mins)

Everybody makes the same mistake in valuation (5 mins)

The explanation of why this shortcut works is as follows:

An investment with compound interest r for t years will double in value when the following equation is satisfied:

(1 + r)ᵗ = 2

Re-organise for t by taking the natural log and treating r as a decimal (e.g. 7% → 0.07):

t = ln(2) / ln(1 + r)

For low interest rates (r less than about 10%):

ln(1 + r) ≈ r

(This is true because of the local linearity of the natural logarithm at values close to 1.) So then:

t ≈ ln(2) / r ≈ 0.693 / r

Which can be rounded for mental arithmetic to 70 / r, where r is a percentage rather than a decimal.

Note: the rule of thumb is good for values of r which are <10%. Sometimes you see people using 72, rather than 70, but this is just because 72 has more integer divisors and is slightly more accurate for higher values of r, e.g. 8-10%. But 70 is good enough, if you remember that it is an approximation.

Benjamin Franklin, The Way to Wealth (1758), derived from Poor Richard’s Almanack essays. The internet also likes to believe that Einstein described compound interest as ‘the 8th wonder of the world’, but there is no evidence he ever said such a thing. As a rule of thumb, you can assume that Einstein or Socrates quotes you find on the internet are bunkum.

I feel like I should say, this is not meant as specific advice about buying into the market today. A lot of people think valuations are inflated, and I have reached a similar conclusion, which could mean that now is not a great time to invest in equities. But I deal with that in a different essay here. The point for this one is more general.

Although I leave it to you to define what ‘needs’ doing now. Obviously don’t delay investments with a high return/payback!

Isn't the better solution to replace the red-light with a roundabout?

So in situations where the consequences are small but the error rate high (lower left quadrant) we empower the decision maker and makes them accountable for their decisions.

Good article Sam!

I was particularly taken by the upfront damage that negative compounding

has. A generally sunnier approach to life is clearly better than the Eeyore “the world is doomed”. It is possibly applicable when talking about climate change and how to address it.